By Julia Beeger, REALTOR® | Oakwyn Realty Ltd. | North Vancouver

By Julia Beeger, REALTOR® | Oakwyn Realty Ltd. | North Vancouver

One of the most common questions I get from buyers, especially first-time buyers here on the North Shore, is this: "Wait, I need a deposit AND a down payment? Are those not the same thing?"

They are not, and mixing them up can cause real stress at exactly the wrong moment in your purchase. The good news is that once you understand how each one works and when the money is due, planning becomes much easier. Here is how deposits and down payments actually work in BC.

The Short Answer

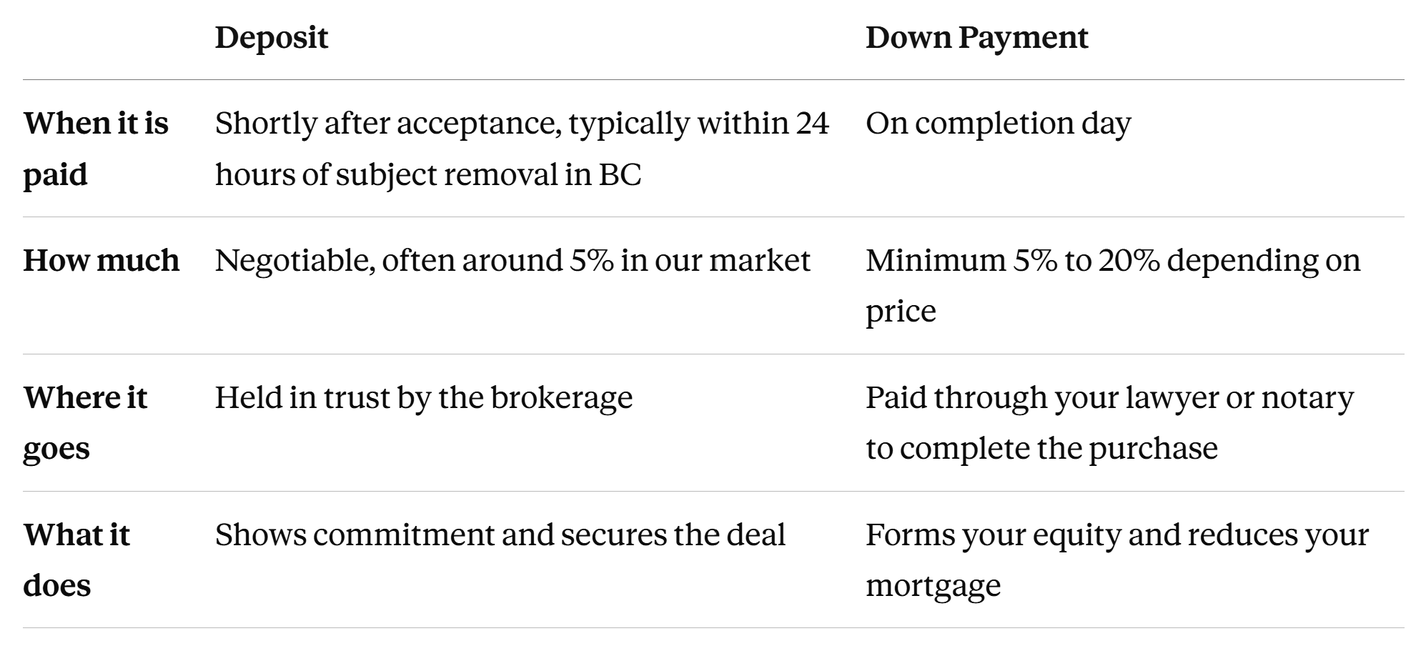

Your deposit is the money you put forward shortly after your offer is accepted. It shows the seller you are committed, and it is held safely in a trust account until the sale completes.

Your down payment is the portion of the purchase price you pay from your own funds on completion day, with your mortgage covering the rest.

Here is the part that surprises people: your deposit is not extra money on top of your down payment. When the sale completes, your deposit is credited toward the total you owe. Think of it as paying a chunk of your down payment early.

How Deposits Work in BC

In BC, the deposit is typically due within 24-48 hours of subject removal, meaning once you have removed your conditions (financing, inspection, strata document review) and the deal has become firm. The amount is negotiable, but in our market, a deposit of roughly 5% of the purchase price is common. In a competitive situation, a larger deposit or handing in a deposit upon an accepted contract before subject removal can signal strength and help your offer stand out.

Your deposit is usually held in trust by the buyer's brokerage. Brokerages in BC are required to hold these funds in regulated trust accounts, so the money is protected while the transaction moves toward completion. Neither the buyer nor the seller can simply take the funds; releasing a deposit generally requires agreement from both parties or a court order.

Can you get your deposit back if the deal falls apart?

It depends on why. If you collapse the deal during your subject period because a condition could not be met, your deposit has typically not even been paid yet, or is returned. But if you walk away from a firm deal without legal grounds, you risk losing your deposit and potentially more. This is exactly why I always recommend buyers only remove subjects when financing is fully confirmed.

BC also has the Home Buyer Rescission Period, which gives buyers of most residential resale properties three business days after acceptance to back out of an offer for any reason, subject to a fee of 0.25% of the purchase price. It is a safety net, not a strategy, but it is good to know it exists.

How Down Payments Work in Canada

Your down payment is your initial equity in the home. The minimum required depends on the purchase price:

Purchase Price | Minimum Down Payment

Up to $500,000 | 5%

$500,000 to $1,499,999 | 5% on the first $500,000, then 10% on the rest

$1,500,000 and up | 20%

If you put down less than 20%, your mortgage will require default insurance through CMHC, Sagen, or Canada Guaranty. The premium is usually added to your mortgage balance rather than paid upfront, and the size of the premium depends on how much you put down.

On the North Shore, where many condos land between $500,000 and $900,000, most first-time buyers fall into that middle tier. As an example, on a $700,000 condo the minimum down payment would be $25,000 on the first $500,000 plus $20,000 on the remaining $200,000, for a total of $45,000.

Deposit vs Down Payment at a Glance

BC also has the Home Buyer Rescission Period, which gives buyers of most residential resale properties three business days after acceptance to back out of an offer for any reason, subject to a fee of 0.25% of the purchase price. It is a safety net, not a strategy, but it is good to know it exists.

How Down Payments Work in Canada

Your down payment is your initial equity in the home. The minimum required depends on the purchase price:

Purchase Price | Minimum Down Payment

Up to $500,000 | 5%

$500,000 to $1,499,999 | 5% on the first $500,000, then 10% on the rest

$1,500,000 and up | 20%

If you put down less than 20%, your mortgage will require default insurance through CMHC, Sagen, or Canada Guaranty. The premium is usually added to your mortgage balance rather than paid upfront, and the size of the premium depends on how much you put down.

On the North Shore, where many condos land between $500,000 and $900,000, most first-time buyers fall into that middle tier. As an example, on a $700,000 condo the minimum down payment would be $25,000 on the first $500,000 plus $20,000 on the remaining $200,000, for a total of $45,000.

Deposit vs Down Payment at a Glance

On completion day, your lawyer or notary prepares a Statement of Adjustments showing exactly how much you owe. Your deposit appears there as a credit, so you only bring in the difference.

A Note on Presale Deposits

Presales work differently, and this is an area I know well from years of working with presale buyers in North Vancouver. When you buy a presale, your deposit goes to the developer's project, usually in stages: an initial amount when you sign, then additional installments over time, often totalling 10% to 20% of the purchase price before completion.

Presales in BC are governed by the Real Estate Development Marketing Act, which gives buyers a seven-day rescission period after signing to review the disclosure statement and change their mind. Your deposit installments are held in trust, but the timeline is much longer than a resale purchase, so your money can be committed for two to four years before you complete. If you are considering a presale, planning your deposit schedule is just as important as planning your down payment.

Saving for Your Down Payment

If you are a first-time buyer, take full advantage of the registered accounts designed to help you:

First Home Savings Account (FHSA): Contribute up to $8,000 per year to a lifetime maximum of $40,000. Contributions are tax deductible and qualifying withdrawals are tax free. If you are eligible and not using one yet, open it now, even with a small amount, to start your contribution room.

Home Buyers' Plan (HBP): Withdraw up to $60,000 from your RRSP tax free for a qualifying first home. You repay it to your RRSP over time.

TFSA: Growth and withdrawals are completely tax free, making it a flexible place to build savings beyond the FHSA limit.

You can combine all three. And do not forget BC's Property Transfer Tax exemptions for first-time buyers and newly built homes, which can save you thousands at completion.

Common Mistakes I See Buyers Make

1. Assuming the deposit is separate from the down payment. It is not. It counts toward your total, but you still need the remaining balance ready for completion day.

2. Not having the deposit liquid. If your funds are sitting in investments or a locked account, you may struggle to produce a bank draft within 24 hours of subject removal. Move your deposit funds somewhere accessible before you start writing offers.

3. Forgetting closing costs. Property Transfer Tax, legal fees, inspection, appraisal, moving costs and strata move-in fees all add up. Budget beyond just the down payment.

4. Making big financial moves before completion. New car loans, job changes, or large unexplained transfers can complicate your financing right when you need it to be smooth.

Let's Talk It Through

Understanding where your money goes, and when, takes so much anxiety out of the buying process. If you are planning a purchase on the North Shore or anywhere in Greater Vancouver, I would love to help you map out your deposit, down payment and closing costs so there are no surprises.

Reach out anytime at 604 306 8746 or julia@juliabeeger.com. And if you are just getting started, grab my free First Time Home Buyer resources at juliabeeger.com/first-time-homebuyers.

Let's Unlock Your Happy.

*Julia Beeger is a REALTOR® with Oakwyn Realty Ltd., specializing in the North Vancouver and North Shore condo market, including presales. This post is for general information only and is not financial, legal or tax advice.

Let's Talk It Through

Understanding where your money goes, and when, takes so much anxiety out of the buying process. If you are planning a purchase on the North Shore or anywhere in Greater Vancouver, I would love to help you map out your deposit, down payment and closing costs so there are no surprises.

Reach out anytime at 604 306 8746 or julia@juliabeeger.com. And if you are just getting started, grab my free First Time Home Buyer resources at juliabeeger.com/first-time-homebuyers.

Let's Unlock Your Happy.

*Julia Beeger is a REALTOR® with Oakwyn Realty Ltd., specializing in the North Vancouver and North Shore condo market, including presales. This post is for general information only and is not financial, legal or tax advice.